While the Covid pandemic feels like a distant memory, its aftereffects still reverberate through the business community. While there are headlines around the country regarding a shift of power back to the employer, and pressure by some companies to get people back in the office full-time, the reality is that many companies have become comfortable with some kind of hybrid policy, generally three or four days a week in the office, with others still opting to work fully remote.

Employer Office Demand Trends Stabilize

Employers have discovered that office sharing and hoteling generally doesn’t work. For anyone coming in at least one day a week, for that employee to be comfortable with their workspace, they require their particular chair, environmental control, amount of natural light, adjacency to certain favorite coworkers or the ability to display friends and family photographs or memorabilia. For the employee to be comfortable coming back and feeling wanted, employers are having to provide a dedicated workspace for every employee that’s now in the office one day a week or more, even though that company may be paying for idle seating capacity that’s sitting vacant up to 80% of the time. As a result, most companies that have people in the office one day a week or more have stabilized their office space utilization.

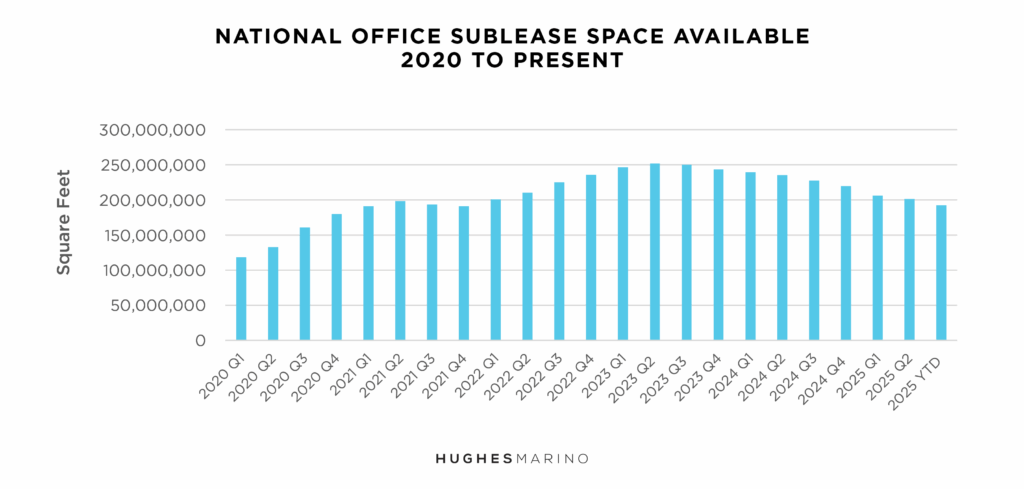

Another factor stabilizing office demand is that those companies that planned to go fully remote already have. Increased supply from companies going fully remote has generally flushed its way through the system. Those companies looking to shed their entire space through subleasing, or a portion of it, have generally already acted on it. This can be measured by the total amount of sublease inventory available in the United States. While still double the historic equilibrium, the amount of sublease space on the market is not growing with significant new offerings. The total amount of office space for sublease nationally has been trending down for over two years. Not only is there little new sublease space being added to the market, but many of these stale subleases have had their leases expire with the space reverting to the building owner, and other value subleases have been successfully subleased.

Office Availability is a Mixed Story

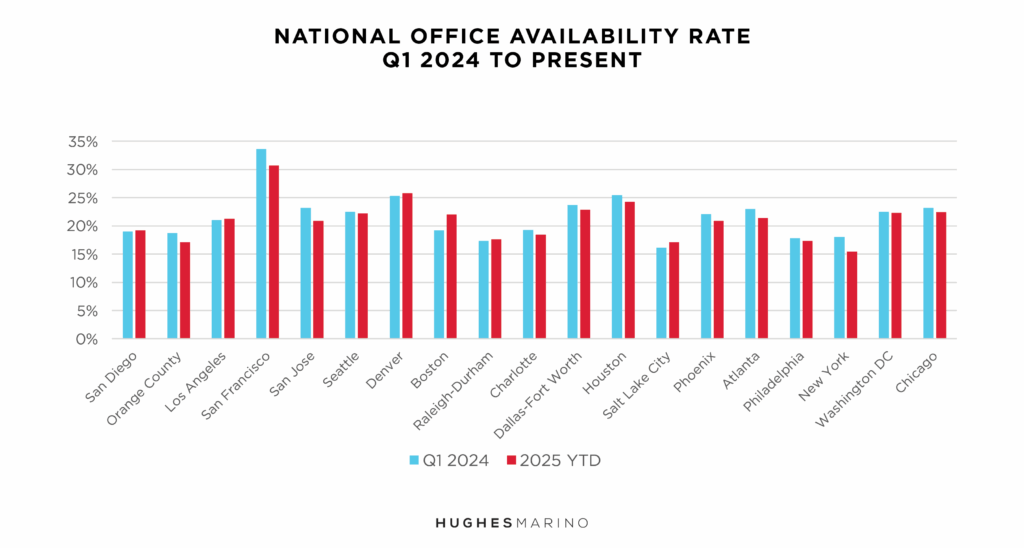

As it relates to availability across the country, it’s a mixed story with a third of the markets getting slightly worse, a third getting slightly better and a third essentially normalized. This is measured below, year-to-date versus 2024, so we can start to understand how things are maturing in a post-Covid reality. Continuing to talk about the office market today as compared to March 2020 is misdirected, as we have entered a market condition that’s never before been seen in history, caused by radical recalibration of how employers and employees have struck a new bargain as to how office space is going to be used—likely lasting for decades ahead.

What’s particularly interesting is how some of the metro markets are moving around more dramatically, whereby San Francisco and New York City have some of the strongest availability declines, much due to growth of AI in San Francisco and the stability of the technology and financial services industries in New York. However, both major markets will still be vulnerable over the next 3-4 years as 10-year leases signed pre-Covid have yet to expire, and a lot of those big companies are sitting on significant excess space capacity. These recent declines in availability, and the office buildings taken off the market for residential conversion reducing the amount of available space, should not be considered a rush back to the office, even though a lot of San Francisco and New York real estate professionals are promoting that narrative.

The biggest increase in office availability can be seen in Boston. That story is driven by Boston landlords and the landlord brokerage community commingling biotech wet lab supply with office space, whereby a large amount of wet lab space has come back to market in the last year, contributing to the spike in office space availability there.

Distress Runs Deep

While the worst appears to finally be behind us for the U.S. office markets, there’s no cause for celebration among building owners and their landlord brokers. The average time that a suite or building sits on the market available for lease has turned into years as opposed to months. With virtually all U.S. markets being above 20%, and many above 25%, it’s a market condition where landlords cannot make money and pay their mortgages in many cases. The wave of foreclosures that began two years ago continue to ripple through the system, with estimates of well over $1 trillion of debt expiring in the next year that all needs to be refinanced, at interest rates that are doubled than what most building owners are currently paying. The office market is so distressed that foreclosures have become quite common, whereby these office buildings are resold at prices ranging from a 70% to 90% discount off their pre-Covid high values. In many U.S. cities, downtown high-rise office buildings are selling for less than $100 per square foot and the buyer is transacting in all cash, as lenders won’t even provide financing for the asset class in many cases. Office markets around the country are generally languishing, yet certain suburban markets have benefited from tenant flight from their adjacent downtowns. Certainly, more amenitized buildings, and those located closest to mass transit, are also outperforming their market peers.

The Extended Tenant Market

The market is in a time of extended volatility where prices will continue to trend down, and concessions trend up. While what’s happening is tragic for building owners and investors, including the insurance companies and pension funds that are invested in much of this real estate, the lenders behind them and municipalities that rely on rental tax or the property tax from their assessed value, this comes at a great time for commercial tenants. As the businesses that are commercial tenants look for opportunities to lean down their costs, and top grade their space to entice their teams back into the office, opportunities abound. Companies facing a lease expiration in the next three years will encounter the softest market that’s been seen in decades and strike great bargains to relocate or retain their space. But to take advantage of these market conditions, tenants need advisors that are aligned with their interests, and not landlord brokers that are promoting some alternative reality to what’s actually occurring. Some landlords today, often because of their capital structure or sheer stubbornness, aren’t able or willing to meet the market. We always find those that do, and act as market makers, not market takers. You should too.

Market statistics provided by CoStar Group.