Because now is a great time to be a tenant

By John Jarvis

I am often asked about where we are today in the commercial real estate market cycle. We can’t trust the headlines, when one headline suggests that the market is suddenly tight again as a result of AI leasing demand, while another headline laments the demise of our urban centers. The honest answer is that there is a lot more happening than the headlines suggest, which led me to develop the Iceberg Market Model. What we read in the headlines is only a small part of the story, with the important details hidden out of view, just beneath the surface.

The Iceberg Market Model

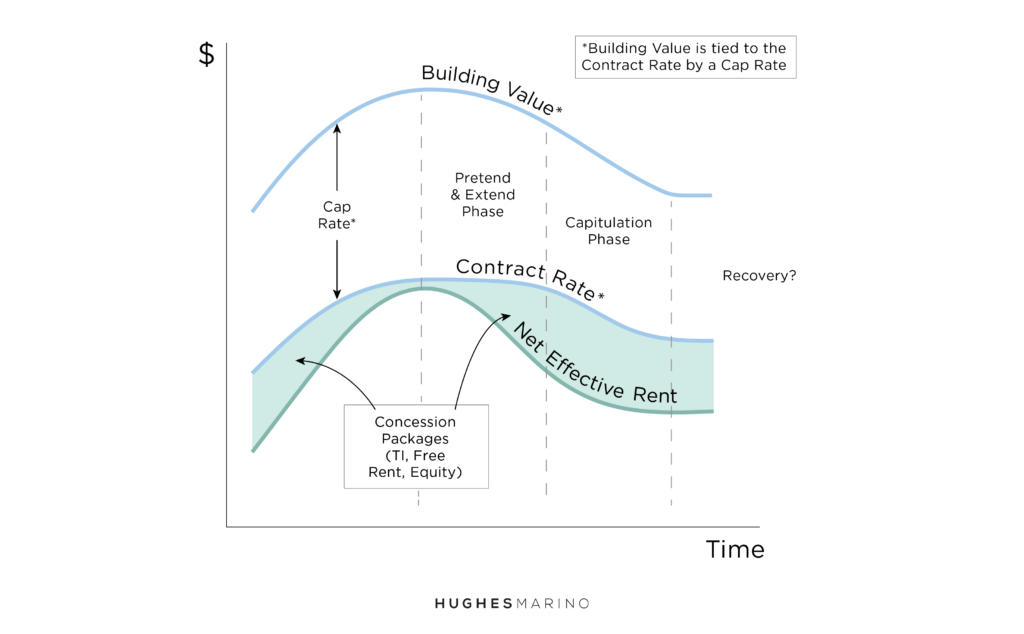

To understand commercial real estate, you need to understand how cap rates determine building values. I wrote about that in an article titled Pennies, Nickels, Dimes and Dollars.

In this article, I’d like to introduce a few other factors that impact building values, including contract rental rates, landlord concession packages and net effective rents. These important details typically aren’t mentioned in market reports, yet they are essential to tell a more complete story about the market cycle. They also help to highlight two distinct phases of a post-peak market in decline, where there is a lag in the decline of asking rates, which leads to (i) the Pretend-and-Extend Phase and (ii) the Capitulation Phase. Let’s dig in.

In commercial real estate negotiations, it is commonly understood that one of the most important deal points for a landlord to protect is the contract rental rate. This is because the contract rental rate becomes the stabilized rent a tenant will pay in the future, and that stabilized rent determines, via the cap rate, the future value of the property. I include the word stabilized because most negotiated transactions include some amount of up-front landlord contributions, also known as concessions, or a concession package, such as a tenant improvement allowance or free rent or a moving allowance. If you include the concession package, you can easily calculate the net effective rent that a landlord will actually receive in a transaction. And the hope of landlords offering these concessions is that a future buyer (or lender) will largely ignore net effective rents (and all those concessions) and instead look at the stabilized rent and the stabilized NOI that a property yields in later years. Put simply: the higher the rent, the more a building is worth, even if the landlord quietly gave away much of that rent in concessions in the early years of the lease.

But what happens when things get really bad? Like the current market for life science lab space, where massive concession packages can now add up to 50% or more of the fictional contract rates? At some point, the fiction has to fold. Nobody is buying the story being sold and the building valuation model shatters under the weight of the massive concessions loaded onto a rickety scaffolding of unsupportable contract rates.

The Pretend and Extend Phase

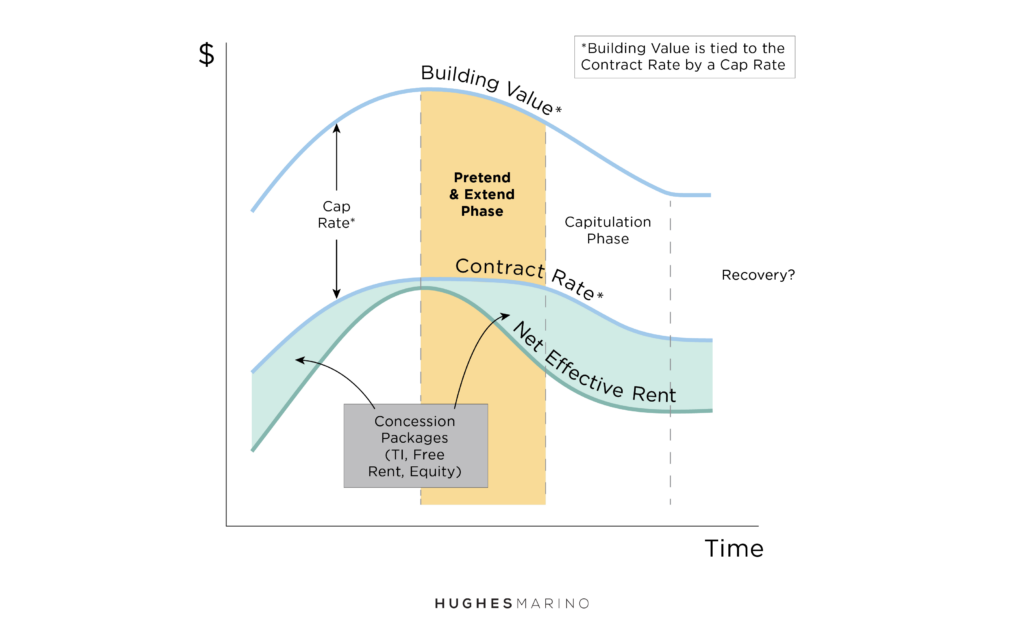

Once a commercial real estate market has peaked and begins to decline, we enter the Pretend and Extend Phase. By which I mean landlords largely pretend the decline isn’t happening and look to “hold the line” on contract rates, while also trying to hold onto their existing tenants by offering ever increasing concessions as incentive on lease renewals. The Net Effective Rents curve actually demonstrates what is happening in the market during this phase, and the result is a widening gap between those unchanged contract rates and the steadily increasing concessions. Until the charade breaks down.

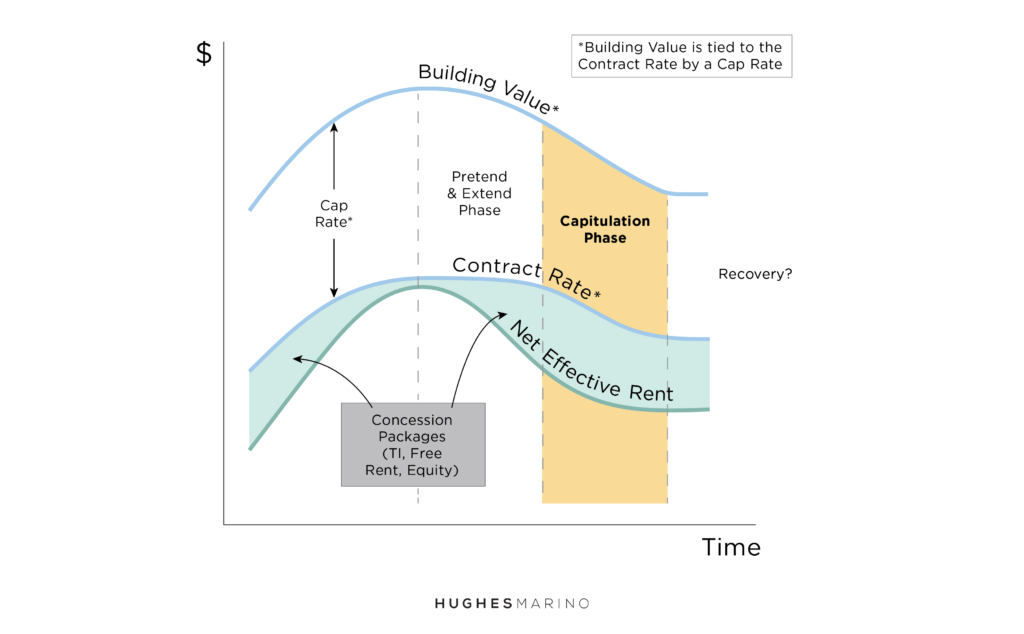

The Capitulation Phase

Capitulation is defined as the act of surrendering, yielding, or ceasing to resist an opponent or a demand. In the Capitulation Phase, landlords no longer try to support the false narrative of building values propped up by elevated contract rates. Nobody’s buying it, so they stop trying to sell it, and instead, they simply lower their contract rental rates. Yes, this will impact the building valuation, but nobody was going to buy the prior, propped-up (fictional) valuation story anyway.

As I write this article at the end of Q2 2026, I see signs that we are now moving beyond the Pretend and Extend Phase and entering the Capitulation Phase, with asking rental rates coming down and pragmatic building owners simply trying to attract quality tenants by transparently meeting the market where it is. Which is smart. And refreshing. Maintaining a fiction over time takes tremendous energy and it isn’t healthy for the market as it disrupts, or at least delays, the naturally occurring market cycle.

Where do we go from here?

Well, up, of course. There are definitely boom times ahead, as the market cycle takes its natural course, like it always does.

But when will that happen?

Now that is a good question. What I can tell you is that the current Capitulation Phase, for all its challenges on the landlord side, is a fantastic time for tenants to negotiate. Landlords are waking up and meeting the market for the first time in years, and that transparency is creating real opportunity for businesses making space decisions today. It’s a great time to be a tenant. And that’s a headline you can trust.