While industrial rents peaked between 2021 and 2023, industrial real estate now enters 2026 almost in free-fall. Industrial landlords and their brokers have been pulling the wool over commercial tenants’ eyes for too long, publishing asking rents that haven’t changed materially since 2023, or not posting rents at all with listing asking prices shown as “withheld” or “negotiable.” But things have in fact changed, and not just on the margin, but radically with how much industrial space is on the market nationally.

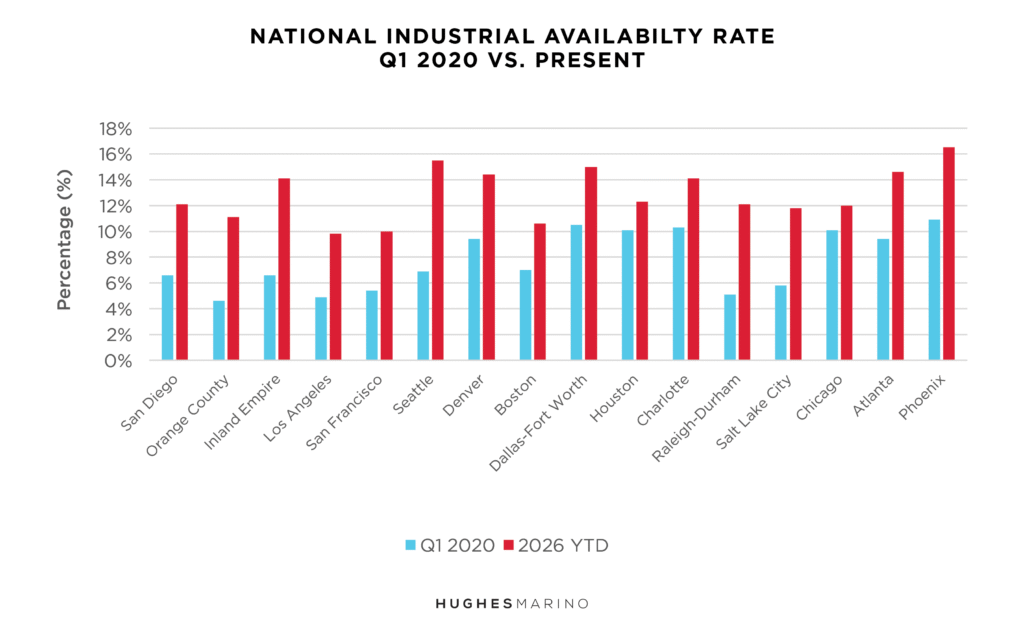

The chart below compares industrial availability in the major U.S. industrial markets from January 2020 against January 2026—the screaming red lines show the greatly inflated supply conditions that we find ourselves in today. Often, landlord listing brokers’ reporting presents quarter-over-quarter numbers that make “vacancy” increases look nominal, but don’t include sublease space, space on the market for lease but not yet vacant, or buildings under construction in their numbers. If you look back to Hughes Marino’s industrial market reports as early as 2023, we predicted that all this was coming…and it’s even worse than we thought it would be.

The above chart illustrates how all of the major industrial markets have boomeranged over the last six years, with every market starting 2026 dramatically higher than 2020 began. Dallas, Denver, Atlanta, Phoenix and Boston are at 150% of their 2020 level; Salt Lake City and the California markets of San Diego, Los Angeles, Inland Empire and San Francisco are all double their 2020 starting points; and Seattle, Raleigh-Durham and Orange County, California, started 2026 higher at 225%, 237% and 241% respectively. Only Chicago at a 19% increase, Houston at 22% and Charlotte at 38% have not been overwhelmed by new construction sitting vacant, subleases languishing on the market and second-generation space coming back to market due to massive downsizings. Commercial developers that have added 1,200,000,000 SF (yes, 1.2 billion SF) could not reasonably expect that they could build what normally would occur over decades in a few years and there not be consequences…but here we are.

Sublease Space Drags Down the Market

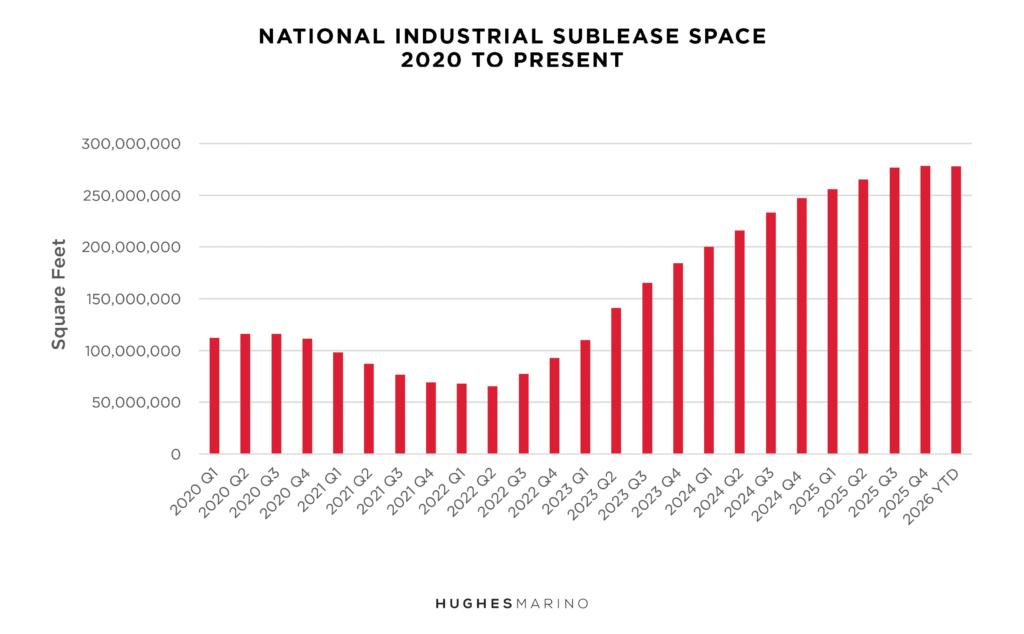

While much of the spike in availability is driven by the excessive amount of new construction nationally, businesses are also retrenching due to overcommitments made between 2021 and 2022. Along with tenants responding to the slowdown of imports in 2025, this has dumped historically high amounts of sublease space on the market throughout the country. Industrial sublease equilibrium over the last few decades has been in the 100M SF range, normally the result of M&A and business changes. The second half of 2022 saw early warning signs of a coming storm for industrial real estate that most landlords, developers and landlord brokers ignored. Sublease inventory then picked up wind in 2023 through 2024, blowing through all historic ceilings. We enter 2026 with a record 278M SF of warehouse and manufacturing space on the market for sublease, which is higher than the 2023 Covid-peak of office space for sublease at 252M SF. By comparison, today there is 100M SF more industrial space on the market in the U.S. than there is office space…and you thought office space nationally was soft!

The Worst is Yet to Come…for Building Owners and Their Brokers

Landlords and their promoting landlord listing brokers are just starting to understand how bad this is, as the downturn has whipsawed them as fast on the way down as the 2020 to 2022 demand explosion did on the way up. Stuck with overpaying for their land and purchasing industrial buildings at record-high prices, many are saddled with promises to lenders and investors that they cannot meet. We are already seeing private owners with low debt levels drop rents and offer massive free rent packages, but the institutional players are locked into a time warp and are struggling to respond to the quickly downward-moving market.

The biggest problem in the market today is that tenants don’t know their bargaining power and often use the landlord’s broker, work directly with the landlord based on some generally flimsy “relationship,” or use some other landlord’s broker to go to market. Riddled with conflicts of interest, steering tenants to broker-preferred outcomes, or simply not understanding the macro market conditions they are operating in today, many brokers get tenants into bad deals. Sadly, there is little transparency in commercial real estate markets, and brokers often revert to “comps” (comparable leases recently signed) to show a tenant what a good deal looks like. But this “followers following followers” is like the old story of the clockmaker setting his clocks to the church bells, and the church bell ringer setting their watch to the watchmaker’s store clocks! Landlord brokers report their collective mediocre leasing results as market information, with statistics bent to the landlords’ benefit, and have little incentive to push back on any of it.

And the Best is Yet to Come…for Tenants

May this be the year that the business owners and executive teams that own and run distribution, 3PL and manufacturing companies take their power back. But to do so, they have to do something differently to expect different results. That something different is to stop trying to do it yourself, or using landlord listing brokers, or purported “tenant reps” that work at landlord “full service” shops, and engage an actual independent tenant advocate that will lead this effort for you and your company’s bottom line.

Frequently Asked Questions

The 2026 industrial real estate market continues to strongly favor tenants, and landlords are now in distress. While institutional landlords and their brokers continue publishing asking rents largely unchanged since 2023, often acting like nothing is wrong, the actual market has shifted dramatically. Availability rates across all major U.S. industrial markets have surged well above 2020 levels, as 1.2B SF of new industrial construction has flooded most U.S. markets, particularly in Sun States and major import hubs like Washington and New Jersey. Simultaneously, industrial sublease space has reached a record 278M SF nationally, more than the peak amount of office sublease space seen during the worst of the pandemic. Tenants who engage the market aggressively in 2026 have a great opportunity to reduce occupancy costs significantly and create unprecedented leverage at the negotiations table.

The markets with the most dramatic availability increases compared to 2020 are Orange County, CA (241% of 2020 levels), Raleigh-Durham (237%) and Seattle (225%). California markets are broadly running at double their 2020 availability levels, including San Diego, Los Angeles, the Inland Empire and San Francisco. Dallas, Denver, Atlanta, Phoenix and Boston are at approximately 150% of their pre-pandemic baselines. The only major markets that have avoided a severe oversupply situation are Chicago (up 19% vs. 2020), Houston (up 22%) and Charlotte (up38%) …yet all trending tenant favorable.

Chicago, Houston and Charlotte are holding the most firm on lease economics, as they are the only major markets where new supply hasn’t overwhelmed demand. However, Dallas, Phoenix, Atlanta and Southern California are at 150–200% of their pre-pandemic availability levels, where pricing is collapsing and deep concessions are to be had, including free rent periods and tenant improvement allowances, even on renewals.

A record 278M SF of warehouse and manufacturing space is available for sublease in the U.S., nearly three times the historic equilibrium of around 100M SF. This sublease glut is driven by two forces: businesses that overcommitted to space during the 2021–2022 demand surge are now downsizing, and the slowdown of imports in 2025, leading many distribution and 3PL operators to shed excess footprint. For tenants, this creates an exceptional opportunity to secure below-market sublease space in nearly every major market.

Effective rents are falling significantly, though published asking rents often don’t reflect this. Many landlords, particularly institutional owners locked into lender obligations, have held asking rents largely flat since 2023, or generally list space as “negotiable” to obscure how far the market has moved. There is little transparency in the U.S. commercial real estate markets. Private landlords with lower debt lead the market in dropping rents and offering large free-rent packages. Tenants who go to market with an independent tenant representative are finding meaningful gaps between asking prices and what deals are actually closing at, particularly in oversupplied California markets, Seattle, New Jersey and the Sun Belt.

Both markets have seen dramatic increases in availability since 2020, Los Angeles and the Inland Empire are each running at approximately double their 2020 availability levels entering 2026. The Inland Empire, which saw an extraordinary construction boom driven by e-commerce and logistics demand, now has some of the highest absolute square footage of vacant and available space in the country. Los Angeles proper faces the additional headwind of high occupancy costs, regulatory complexity and continued economic softness. Both markets represent strong negotiating opportunities for tenants, particularly those whose leases expire in 2026–2028.

Industrial tenant representation is a specialized discipline distinct from general commercial brokerage. Most brokerage firms operate as “full-service” shops, representing primarily landlords with tenants as a byproduct of their landlord services model. This is a structural conflict of interest that steers tenants toward brokers’ landlord-preferred outcomes and sets up rich financial conflicts of interest whereby the landlord broker tries to make both side of the commission. In a market as complex as 2026, where asking rents are artificially held high while actual deal economics have shifted dramatically, an independent tenant-only advocate is essential to capture the savings that can be obtained today. Hughes Marino specializes in representing tenants and occupiers, not landlords, across industrial, office and lab/research space nationwide. Companies consolidating their footprint, that still need to lean down or that are approaching lease expirations should engage an actual tenant rep firm, versus someone posing as a tenant rep at a full-service landlord company, as the negotiating window is open now.

With 278M SF of industrial sublease space on the market nationally, short-term 1–3-year warehouse options are unusually abundant in 2026. Sublease space typically offers below-market rents, pre-built infrastructure and flexible terms, since the sublandlord’s priority is cost recovery rather than profit. The challenge is that much of this space isn’t actively marketed on public platforms, and the best deals require a tenant’s broker with current market intelligence. Companies looking for short-term or flex industrial space should work with an independent tenant representative who tracks sublease availability across markets, rather than relying on listing sites that often show outdated pricing and incomplete inventory.

Market statistics provided by CoStar Group.