Five years post-Covid and the ripple-effect of the damage is still working its way through the San Francisco office market. Companies for the most part have adjusted to their new normal by implementing hybrid and remote schedules, and many tenant leases (and most importantly, subleases) have already expired, allowing for the opportunity to reset their footprint accordingly.

Artificial intelligence startups are increasingly electing to adopt in-office work policies (up to 4-5 days in-office), using their cohesive, collaborative and “fail fast, pivot” mentality as a recruiting tactic. In the past two quarters, there has also been an uptick in larger lease transactions (greater than 50,000 SF) which outside of a small handful of companies such as OpenAI, had been a dormant part of the market from a demand perspective.

Despite this, there’s still more volatility as some very large law firms and other professional service firms still have another two or three years left on their pre-Covid long term leases. These coming lease expirations will create future incremental increases in availability for another two years as those companies continue to shed space. Notwithstanding, we are formally reporting that the worst occupancy effects of Covid are in the past.

Value Reset and Distressed Building Sales

As the vacancy rates skyrocketed and the Federal Reserve’s interest rate tightening policy was implemented, the result has been a sharp correction in building values across the country, yet given how overheated San Francisco’s market had gotten before Covid, the declines seen here have shocked many in the commercial real estate industry. For buildings that last traded hands between 2016-2019, 70-80% declines in value have become the norm with new owners, who are local by in large, acquiring for less than the debt amount assumed by the prior lender.

Earlier this year at Market Center, a 1M SF two-building Class A project in the heart of the Financial District, Flynn Properties purchased 555-575 Market for around half the loan value which Paramount Group had defaulted on. This example is the first of the Class A variety in the city and we expect there will be more to come over the coming years. As covered in a recent article, the majority of this distress is happening behind the curtains and out of the spotlight. As more of this distress works its way through the capital markets and more new owners acquire quality buildings for a fraction of the prior values, there will be additional downward pressure on rental rates.

Supply and Demand Imbalance Based on Size

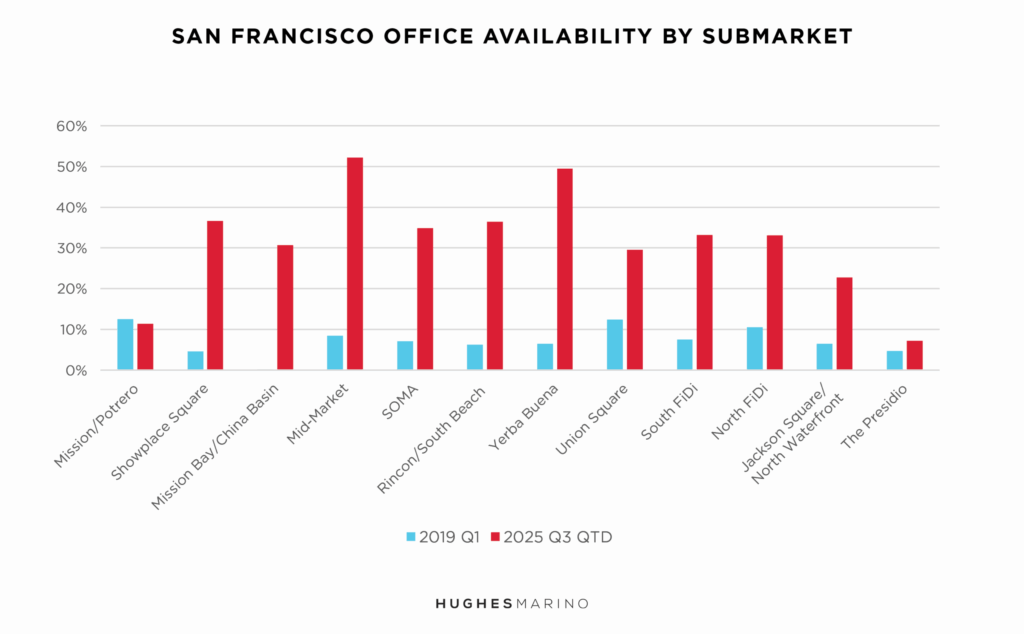

While office availability remains north of 35% across the city, over half of the vacant 35M SF is made up of opportunities 20,000 SF or greater. Given the high cost of construction and risk implicit with altering larger full floor spaces speculatively before interested tenants come calling, many owners have been reluctant to meet the market where the demand is most active—in the sub-7,000 SF range. Furthermore, supply has remained most robust in the South Financial District, Yerba Buena, SOMA, Mid-Market and Union Square submarkets, while the demand trends are shifting north. Jackson Square, in particular, has seen a tightening with availability around 15% as strong demand from startups, design firms and venture capital alike have taken to the creative brick and timber aesthetic and relatively well-kept streets as compared to parts of SOMA which were more in vogue pre-Covid.

The most active tenant requirements in the market currently are from early-stage AI companies still in or just coming out of stealth mode. They are most frequently seeking furnished space for 15-20 people and prefer short term leases. This demand has caused a competitive dynamic on high quality and well-located spaces—and has compelled many owners to assume the cost of furnishing direct lease opportunities. Furthermore, six years ago when owners would require a minimum of a five-year lease, many now are acquiescing to as short as two years of term.

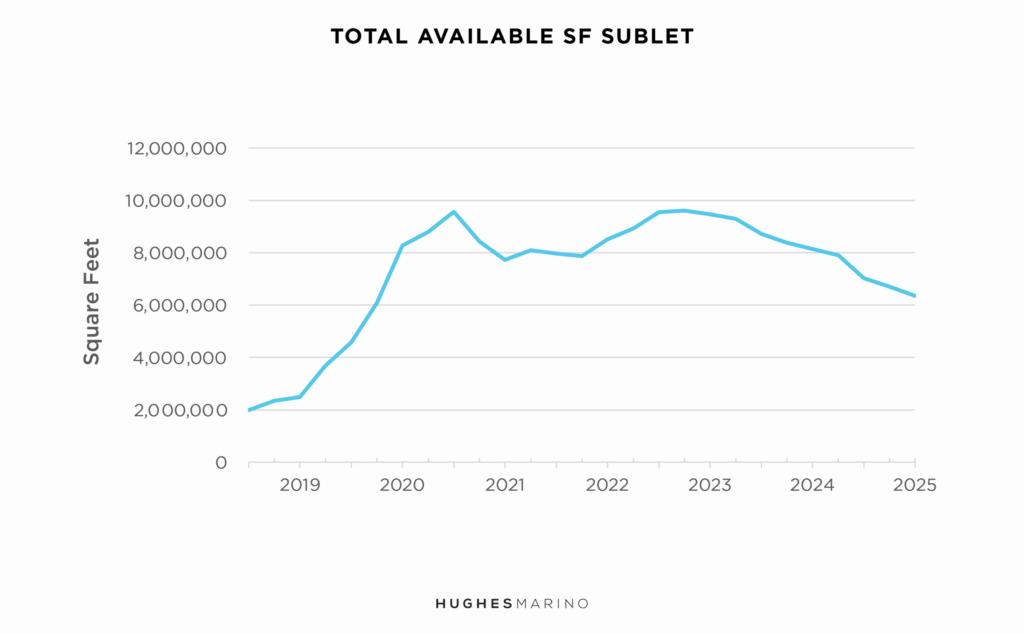

Sublease Space is Trending Downwards as Leases Expire

San Francisco saw a dramatic uptick of sublease space available from 2020 to 2021 as tenants concluded they would not be coming back to the office, or that they would be coming back much smaller. As companies began returning to the office, some of that space was withdrawn from the market, and the good sublease deals were picked off by tenants looking to bring their teams back together.

By the start of 2022, employers began to understand that remote and hybrid working was here to stay, or simply refused to come back into the office, resulting in record high levels of office sublease space being put on, and then lingering on the market. A year ago, this supply started bleeding off, as those subleases that had been on the market for 2-3 years let the leases expire, and the space reverted back to the landlords. The reality is that tenants’ opportunities to pick off a value sublease are starting to dissipate, and oftentimes, tenants in the market cannot find an acceptable sublease with at least two years of remaining term and also meets their needs.

Looking ahead, office space availability will remain strong and prices will remain soft, as the availability rates and number of choices that tenants have are just too large to conclude anything else. Tenants are going to enjoy some of the lowest office rents they’ve seen in 25 years for many years to come.

Market statistics provided by CoStar Group.