By David Marino

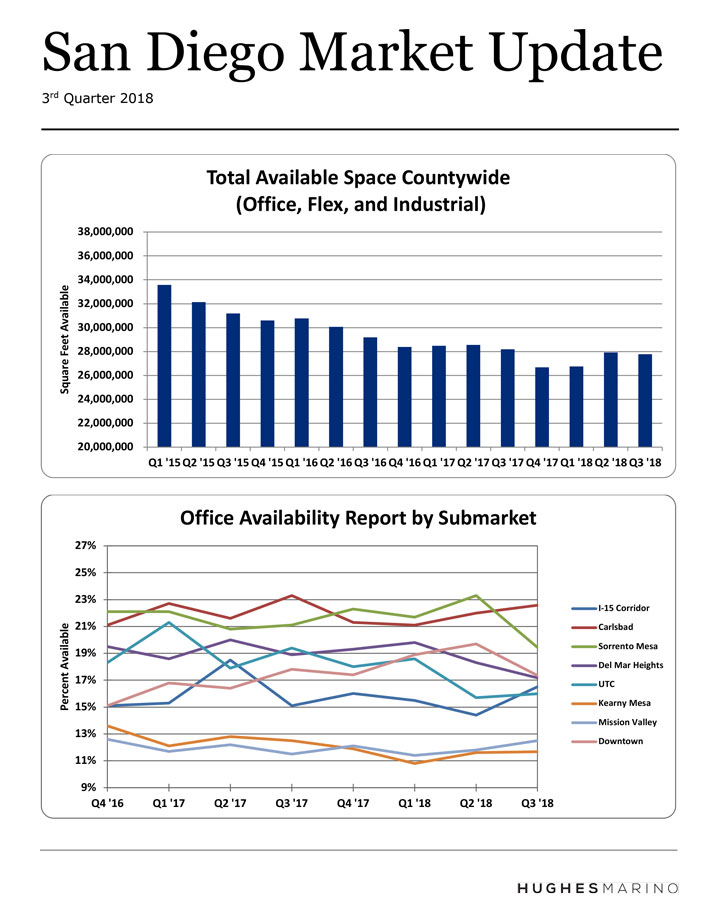

This third quarter of 2018 ended with mixed results countywide at the macro level for combined office, lab and industrial space. Only 158,000 square feet of net space came off the market in 3rd quarter, leaving the county year to date with 1.1 million square feet of increased square feet availability since the beginning of 2018. In past years where we have seen anywhere from 2 to 5 million square feet of space being absorbed countywide, 2018 is the first negative year that the San Diego region has seen in this eight-year economic recovery.

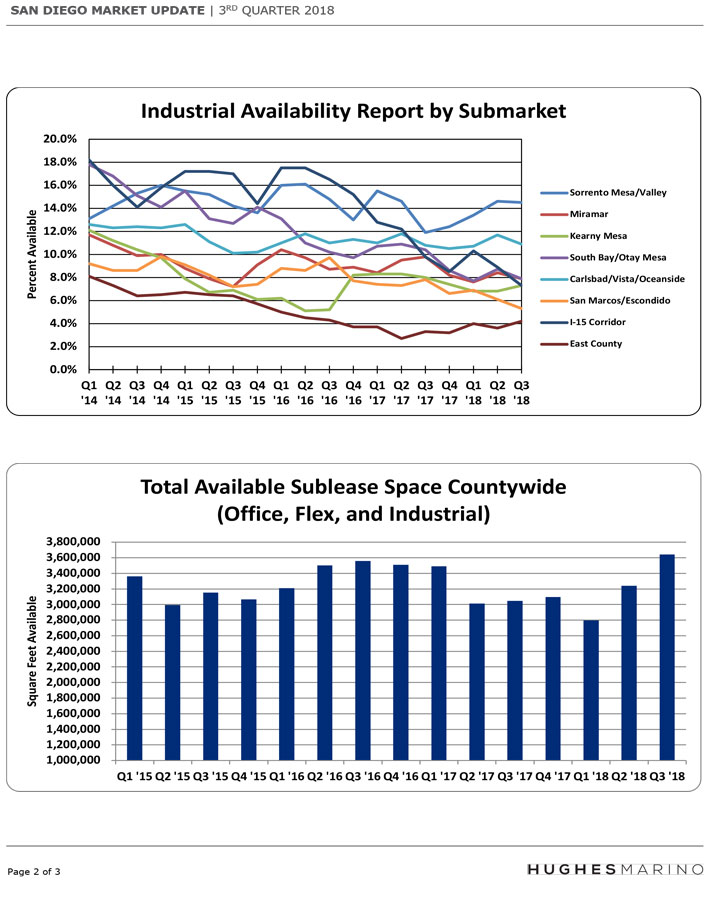

In the year leading up to prior economic recessions in both 1999 before the tech wreck, and in 2007 before the residential real estate mortgage implosion, we saw rapid increases in sublease availability in the region. Of great concern is that this past third quarter was the second quarter in a row where total sublease inventory increased substantially, with another 402,000 square feet of net sublease space added to the market on top of the net 442,000 square feet that was added in the second quarter of 2018. We will track this carefully throughout the balance of the year, as if we see another significant increase in sublease inventory in the 4th quarter, it could be a leading sign of an economic downturn that would come as soon as Q2 or Q3 of 2019. Let’s hope this isn’t the case and that 2018 finishes out with this sublease inventory being absorbed by other growing tenants and that other companies don’t continue to shed existing facilities that have come to market from M&A or business downturn reasons.

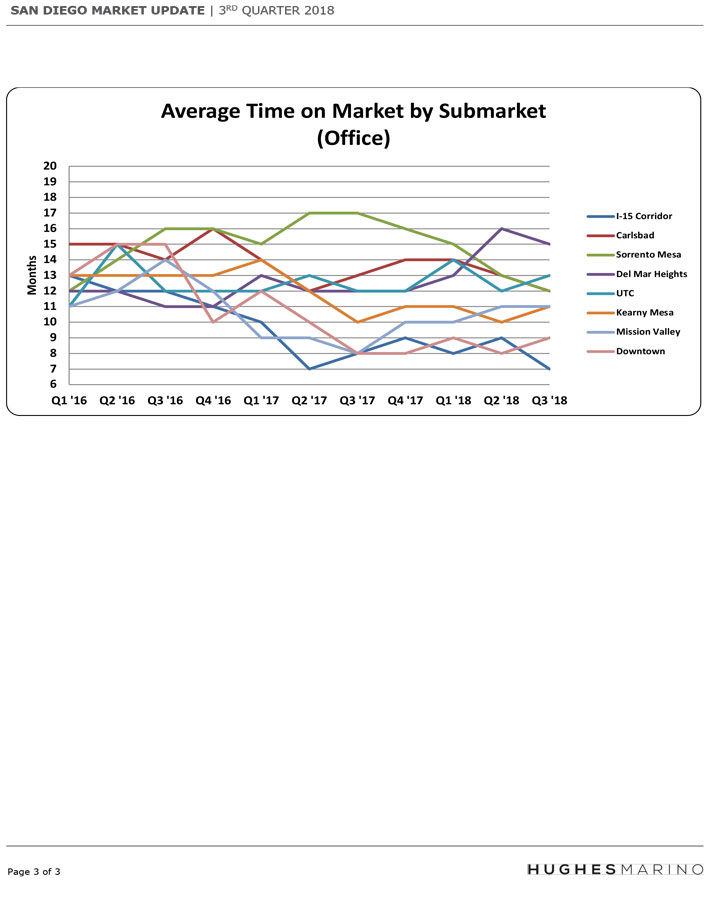

Total office availability continues to have a severe hangover in markets like Carlsbad, Sorrento Mesa and Del Mar Heights, with availabilities at 22.6%, 19.4% and 17.2% respectively. The most dramatically improved market is UTC where availability has gone from 19.4% to 16% in the last year, and we are starting to see lack of availability of large blocks of space over 15,000 square feet and upward pressure on rents. The I-15 Corridor, which was so strong from 2015 to 2017 as companies moved from more expensive and congested coastal submarkets like Del Mar Heights and Sorrento Mesa, has seen a surprising uptick in availability going from 15.1% to 16.5% in the last year. The average time on the market for some office submarkets is getting better and some are getting worse. Sorrento Mesa declined from 17 months to 12 months which is the most improved in the region, meanwhile Del Mar Heights, the most expensive market in the county, has moved from 12 months to 15 months in the last year. We are starting to see Del Mar Heights lose its luster as some of the law firms in that market already begin to downsize and rental rates that now range from $4.50 to $5.50 “net of electricity” are becoming unaffordable for most companies. We believe that prudent tenants will look south to options in Sorrento Mesa and UTC particularly if 2019 becomes a belt tightening year.

Downtown San Diego is a tight market, with the only large blocks of availability in undesirable buildings or with undesirable landlords. There will be a glut of new office space online in the next one to three years–which Downtown desperately needs. We represent most of the tech companies in the region–and the jury is still out on whether these tech companies want to pay some of the highest rates in the county for buildings like Horton Plaza (which is being reconfigured to house “creative office”). Downtown is one of the most fickle markets due to the high cost of parking. As rates rise above $3.00 per square foot, tenants start to look elsewhere in San Diego due to the added cost of parking in downtown. As rates rise, we’ll see availability eb and flow and companies continue to move in and out of the city due to added costs like parking.

As it relates to life science facilities, there is tremendous excitement around the industry’s success in raising billions of dollars in the last couple of years which has fueled job growth and demand for space. There are a couple of million square feet of new lab projects in the pipeline that will be delivered in the next three years and developers are hoping that the capital markets and demand holds to see these projects to their successful conclusion. However, if there are storm clouds on the horizon for any reason, these projects are going to be put on hold or put into jeopardy.

As for industrial space, the market continues to be white hot. The Central County has run out of developable industrial land, and existing buildings over 20,000 square feet are generally in high demand. Warehouse space that used to lease for $.45 NNN a decade ago, now leases for $.85-$.95…if you can find it. Other than for Sorrento Mesa with availability of 14.5%, and Carlsbad at 11% due to some new construction and sublease inventory, all of the other regional markets are between 4%-8% availability, and healthy. The once soft Otay Mesa and South Bay submarkets are seeing competition for buildings, and new construction pre-leased before construction is even finished.

In conclusion, while the major metro areas throughout the rest of the state (Los Angeles, Orange County and Northern California) appear to be strong and stable, there are some serious question marks about the condition of the major office markets of San Diego County and the strength of the regional economy as a whole at this time. We will hopefully have better news to report at the end of the year…but if we don’t, 2019 might be setting up for a wild ride.