Five years post-Covid, the Dallas-Fort Worth (DFW) office market is showing signs of stabilization as the shift to remote and hybrid work (2-4 days in-office) has largely settled. Most tenants have already adjusted their footprints as pre-Covid leases expired, allowing companies to right-size. The leasing activity in Q1 and Q2 of this year reflects this, with approximately 11.1M SF leased across major submarkets, driven by a “flight to quality” toward modern, amenity-rich spaces. However, upcoming lease expirations for larger tenants in finance, tech and professional services over the next 2-3 years will likely increase availability, particularly in Dallas CBD, Las Colinas and Frisco/The Colony. We report that the worst occupancy impacts of Covid are behind us, with tenant-favorable conditions persisting due to elevated availability.

Dallas CBD: A Soft Central Business District

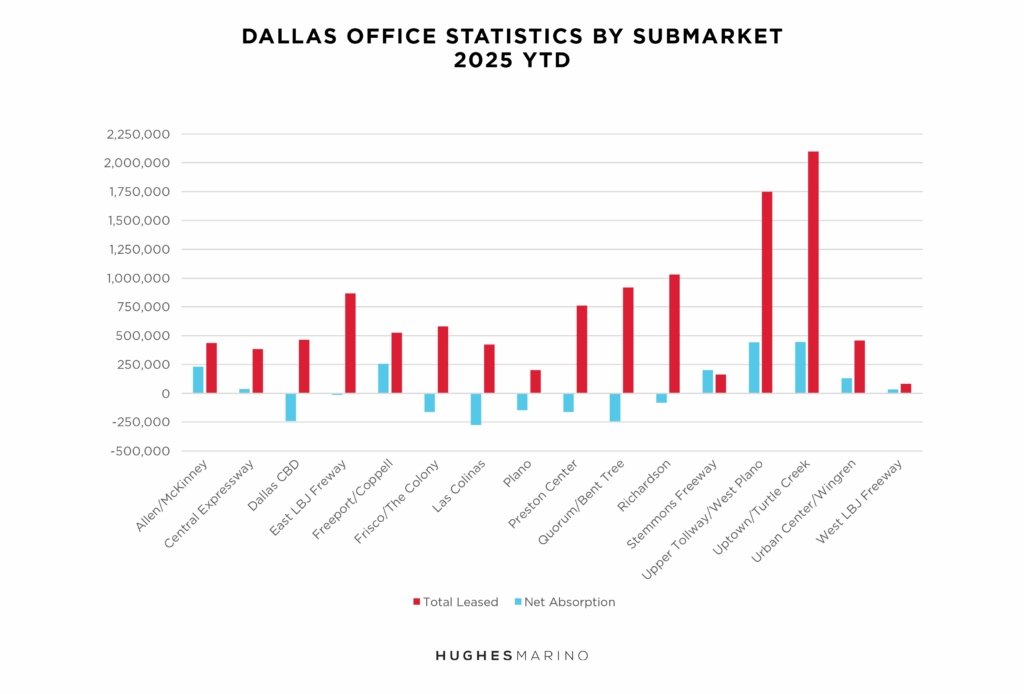

The Dallas CBD remains one of DFW’s softest submarkets, with high availability driven by remote work, cost pressures and parking challenges. The 2025 YTD data shows negative net absorption of -238,115 SF, though 465,002 SF was leased, indicating some demand for smaller spaces (20,000-50,000 SF) by professional services firms. Pre-Covid availability was around 20-22%, but post-Covid tenant relocations to suburbs and downsizing have pushed availability even higher. Older buildings struggle against newer suburban developments, and speculative pre-Covid projects have failed to attract tenants. Conversions to multifamily or mixed-use are under consideration for underperforming assets, which could reduce office supply. Tenants can leverage high availability for competitive rents and generous concessions like free rent and tenant improvement (TI) packages.

Submarket Trends: Availability and Leasing Activity

The 2025 YTD data highlights varied performance across DFW submarkets:

Uptown/Turtle Creek: A standout with +446,261 SF net absorption and 2.1M SF leased, driven by premium amenities and proximity to talent. Availability remains moderate, but asking rents are the highest in DFW ($56-$66/SF), supported by 2.15M SF under construction (69% of DFW’s pipeline). Tenants seeking high-image spaces face premium pricing but can still negotiate concessions.

Upper Tollway/West Plano: Strong with +441,811 SF net absorption and 1.75M SF leased, reflecting demand for modern suburban offices. Availability is lower than average, but tenants can secure deals around $30-$35/SF with significant TI allowances.

Freeport/Coppell: Positive at +256,854 SF net absorption and 526,698 SF leased, benefiting from logistics proximity. Availability is moderate, offering tenants cost-effective options ($25-$30/SF).

Las Colinas and Quorum/Bent Tree: Negative absorption (-273,893 SF and -241,786 SF, respectively) signals higher availability. Tenants can capitalize on soft conditions for below-market rates and flexible terms.

Richardson and Plano: Mixed performance, with Richardson leasing 1.03M SF but negative absorption (-82,734 SF), and Plano at -145,614 SF net absorption with 201,679 SF leased. High availability offers tenants leverage for deals under $30/SF.

Across DFW, availability rates above 15% indicate tenant-favorable markets, with submarkets exceeding 20% (e.g., Dallas CBD, Las Colinas, Frisco/The Colony) offering the best opportunities for low rents and concessions.

Uptown/Turtle Creek: A Premium Outlier

Uptown/Turtle Creek defies softer trends, with strong leasing (2.1M SF YTD) and positive absorption (+446,261 SF). Its walkable amenities, modern buildings and talent access drive demand, but high asking rents ($56-$66/SF) are propped up by a few dominant landlords offering substantial free rent and TIs to maintain face rates. Nearby Preston Center mirrors this, with 762,088 SF leased and limited availability, pushing rents to $50-$53/SF. Tenants can still find value in adjacent areas like Upper Tollway, where availability allows more competitive pricing.

Sublease Space: Declining Opportunities

Post-Covid, DFW saw a surge in sublease space (peaking at 12M SF in 2022) as tenants downsized. By Q2 2025, sublease availability has dropped significantly (down 33.8% from 2023 highs to ~8.1M SF), as leases expire and space reverts to landlords. The 2025 YTD data shows robust leasing (11.1M SF total), but sublease deals under $25/SF are becoming scarce as quality spaces are absorbed. Tenants seeking short-term, cost-effective options must act quickly, as remaining subleases often have less than two years of term.

Outlook: Tenant Leverage Persists

Office-using employment in DFW has grown modestly to ~1.2 million jobs (up 0.5% YOY), but below pre-Covid rates. With availability rates above 15% across most submarkets, tenants can secure some of the lowest rents in 25 years, especially in high-availability areas like Dallas CBD and Las Colinas. Concessions remain generous, and sublease opportunities, while declining, still offer value. Tenants should act strategically to lock in favorable terms before future lease expirations add more space, particularly in 2027-2028.

Market statistics provided by CoStar Group.