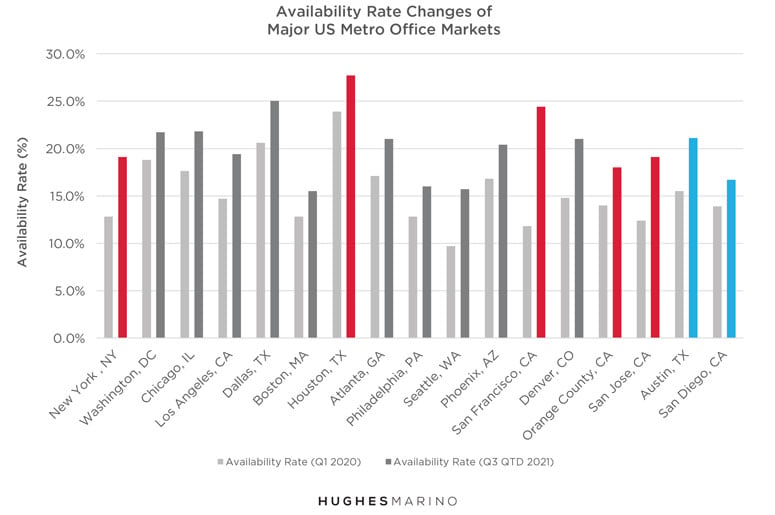

COVID-19 had the most dramatic effect on increasing office availability rates in 2020 than any time since the 2000 Tech Wreck. While the Tech Wreck availability uptick was related to a collapse of the financial markets and the tech sector generally, whereby hundreds of millions of square feet of office space across the country came back to market through tenant defaults, the 2020 increase was caused by corporate America either relinquishing its office space as leases expired or putting unprecedented amounts of office space on the market for sublease. The chart below identifies the major US office markets pre-pandemic availability rates as compared to today.

While most metro markets are still modestly increasing in availability, year to date (YTD) most office markets have not increased by more than half a percentage point. Those highlighted in red are the most negatively affected by companies still shedding office space including New York City, Houston, San Francisco, Orange County and San Jose, all of which have increased by more than half a percentage point YTD. Austin and San Diego, highlighted in blue, are the only major metro areas where availability has actually gone down more than half a percentage point YTD, showing that the worst might be behind only in these markets.

Some of the tightest pre-pandemic markets in the country have been hit hardest, with San Francisco availability more than doubling since the pandemic began, New York City going up almost 50%, San Jose rising 54%, Denver growing 42% and Seattle increasing by 62%. Generally suburban office space has a higher occupancy rate than the central business district where commuters take mass transit to get to work, potentially exposing people to COVID-19 during their commute. High-rise buildings where tenants are required to take often crowded elevators, creating the perception of additional COVID-19 exposure risks, generally have a lower occupancy rate.

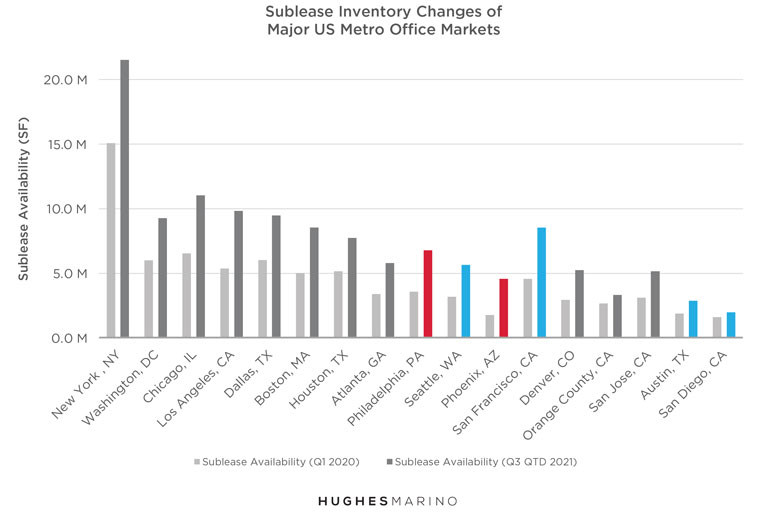

What is unprecedented in the commercial office market is the flood of sublease inventory that has come back to market during COVID-19. In this COVID-19 driven downturn, corporate America has remained financially healthy and has generally been performing on their lease obligations, putting excess space on the market for sublease in lieu of the defaults we saw during the Tech Wreck and 2008 mortgage crisis. Most metro areas are hitting records with the millions of square feet on the market for Sublease, and the square footage increase from pre-COVID to YTD are reflected below. Highlighted in red are those markets continuing to get worse in 2021 where YTD sublease inventory increased by more than 10%, including Philadelphia and Phoenix. Highlighted in blue are those markets that are trending positively whereby sublease inventory is going down by more than 10% year to date.

One would think that sublease inventory would have been declining by now and that the worst is behind us. However, what we are seeing is that more companies are reaching the conclusion that they are not coming back to the current footprint they have, and new subleases come to market every week as a result. Depending on the COVID-19 Delta variant’s impact on health conditions for the balance of the year, this total glut of office sublease inventory will persist well into 2022 and 2023, continuing to be a thorn in the side of all landlords that have to compete with their own tenants looking to dump space.

The forecast is for availability rates to continue to go up for the next three years in most major metro areas. Since the pandemic began, only approximately 15% of all office leases in the country have expired. As we go into the next three years, another approximately 50% of office leases will expire around the country, allowing tens of thousands of commercial real estate tenants to reassess their footprint requirements. Consensus is that remote working and hybrid models are here to stay for most companies in most industries, and that means that most tenants of all sizes are going to need less space when their lease expires. Many companies can get by with 20% to 30% less space than they lease today. As companies relocate or downsize in place to less space, the net result is that landlords are going to be handed back tens of millions of square feet of office space across the country every year. It’s not something anyone’s going to notice in any particular quarter, but there is going to be a long three-year drift to the bottom in most metro markets.

Marketing statistics provided by CoStar Group.